The start of what may be a stream of rising interest rates as the Federal Reserve fights high inflation has stock investors jittery, and rightly so.

The more bond yields rise, the more likely income-seeking investors will move money out of the stock market.

But this is also the part of the interest-rate and economic cycles during which banks’ profits rise. And bank stocks’ valuations to earnings have been declining. That sets up a potentially fruitful scenario.

In an interview, Sam Peters, a portfolio manager at ClearBridge Investments, outlined the case for buying bank stocks. ClearBridge is based in New York and has about $208 billion in assets under management. Peters co-manages the ClearBridge Value Trust

LMNVX,

and the ClearBridge All Cap Value Fund

SFVYX,

He is based in Baltimore.

Peters pointed to increasing loan demand, improving profitability as interest-rate spreads widen and a decline in bank stock valuations so far this year.

The Fed provides a tailwind

Let’s begin by looking at interest-rate spreads. Banks’ main funding source is deposits, and their best way of making money is by lending out the money. If a bank can’t make enough loans, it will buy bonds. The problem with bond portfolios in the current environment is that as interest rates rise, bonds’ market values decline, and resulting markdowns reduce banks’ profits.

But on the loan side, rising interest rates have benefits in a strong economy:

- Payments on loans with adjustable rates increase.

- Commercial loans, which tend to have relatively short maturities, are renewed at higher interest rates.

Meanwhile, in its fourth-quarter Banking Profile, the Federal Deposit Insurance Corp. said loan volume was growing across “most major loan types.” Looking ahead, Peters expects commercial borrowing to increase with the end of federal stimulus programs that propped up the economy during the coronavirus pandemic.

Banks keep deposit rates low

The Fed made its first move last week, increasing the target federal funds rate to a range of 0.25% to 0.50% from its previous target of zero to 0.25%.

You may have seen some headlines about a flat Treasury yield curve or even an inverted yield curve, as an advance signal that a recession is coming. It may even take an eventual recession to tamp down inflation sufficiently for the Fed to achieve its 2% target for price increases in the U.S.

At the end of business on March 23, the yield on 10-year U.S. Treasury notes

TMUBMUSD10Y,

was 2.32%, which was the same as the yield on three-year notes

TMUBMUSD03Y,

according to the Treasury Department’s daily yield curve. The curve was indeed inverted with yields of 2.34% on five-year notes

TMUBMUSD05Y,

and 2.37% on seven-year notes

TMUBMUSD07Y,

But for the banks, the situation is completely different.

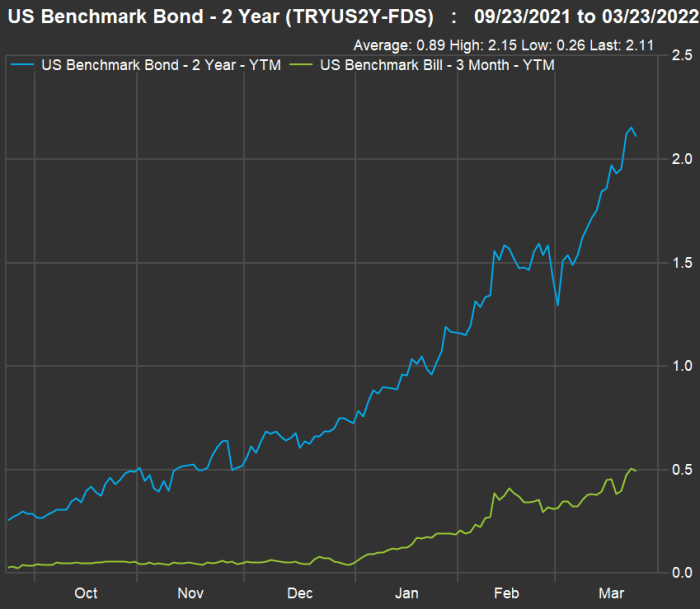

In a world that continues to be awash with cash, banks don’t need to pay much for deposits. Peters said a good proxy for banks’ spread between their cost of deposits and loan rates is a comparison between yields on three-month Treasury bills

TMUBMUSD03M,

and two-year Treasury notes

TMUBMUSD05Y,

Here’s how those rates have moved over the past six months, according to data compiled by FactSet:

FactSet

At the end of March 23, the yield on two-year Treasury notes was 2.11%,…

Read More: The Federal Reserve’s big policy shift points to good times for bank stocks

{kind=link}